The year ahead

I hope you all enjoyed a well-deserved holiday with family and friends. I think of trading like any performance sport, you can’t be working to the bone all day every day, your body and mind needs time to rest and recover to operate at peak efficiency. Hopefully the low volume December drift afforded you the time to do that. But now it’s officially the dawn of a New Year. I personally had my best year ever in 2023, as I reflect on the last day of the year, I see so many areas and aspects where I have improved as a trader, which makes me so excited for the future. I am expecting to continue that trend in 2024 and couldn’t be more excited to take another leap forward with you guys.

I want to begin with a high-level overview of where I see the trajectory of asset markets in the next 12 months. This is subject to change as we are provided with new information, but also I expect some major themes outlined now to be consistent market drivers throughout the entire year.

The Fed

Let’s start off with the FOMC. Markets are essentially at all time highs as of writing, and much of that can be attributed to the ostensible end of the Fed’s hiking cycle. A lofty 6 cuts are currently being priced in for 2024. I personally think that is on the high side. I think much of the price action, especially in 1Q/2Q will be assets moving in accordance to the amount of easing that Fed Fund Futures are pricing in. I think cuts right now are basically a sure thing, but I see 3-4 as more realistic rather than 6. I do think Powell intended to float that trial balloon into the markets consciousness and see how things developed. I also agree that policy is perhaps a bit too tight right now. With CPI consistently falling throughout the entire year, holding rates steady is de facto tightening. There certainly are two sided risks to the economy right now. However, the market’s animal spirits took over and went a bit overzealous on rate cuts pricing.

I disagree that it was a policy error, I think monetary policy and especially forward guidance is an especially blunt tool. The Chair can’t exactly go out and say exactly 4 cuts are priced in next year when really he nor anybody else on the planet really knows what will happen in the economy between now and 2025. So what he did, and I think it makes perfect sense, is to float that idea, whisper in the markets ear so to speak and let it marinate for a bit. Fully knowing, and expecting to have to talk the market down, readjust expectations and recalibrate throughout the year. I imagine it to be like golf. First you have to get the driver and the woods out, to get the ball in the general vicinity of the hole. You may overshoot, or undershoot. Once you are within spitting distance, you then get the putter out and go to work like Tiger at the 05 Masters. Powell just hit a long stroke for 200 yards to get the ball (rates pricing) in the general range he wants, and in the beginning of the year is when he gets the putter out and really tries to dial in market expectations to what he deems is appropriate for the time.

Another clue to the markets over exuberance is having Fed’s Williams come out to try and walk back some of the latest rate cut euphoria very shortly after the Dec FOMC.

This isnt Game of Thrones. If William’s came out to say that, it was with Powell’s blessing and explicit approval.

I think what will be very key in January is the NFP jobs report in the first week of Jan as well as the CPI later. This is still a very data dependent Fed. If not, the FOMC at the end of the month is where I think we likely see Powell try and guide market pricing to something a bit lower than 6 cuts.

Bonds

We ended 2023 with a bond rally for the decades. TLT saw about a 20% rally in 2 months from the $83 low. This is not a meme stock, that’s a historic move when accounting for the relatively low implied volatility. Yields went from 5% to 3.8%. I can see yields in the 3-3.5% range later this year, but as we begin 2024 I think we may see some profit takers and natural sellers in treasuries. Everything that was dragging down fixed income in 2Q/3Q of 2023 is still present. Things arguably have gotten worse not better. There is still no end in sight for the tsunami of issuance in 2024. The US is spending like its in a crisis. I wont come out and say inflation is coming back as a certainty as in ‘66-’82, but I also wont say that it has been defeated yet either. Until the market is reasonably certain that price stability has been restored, we will keep seeing elevated rates volatility and that likely means some vicious rallies in yields (sell off in bonds).

Equities

Now of course onto my favourite topic, stocks and the SPX. It’s important to know whats happening with FOMC and rates pricing, as well as the bond market as they are the major drivers of equities right now. As we kick off 2024 in the 4800s, I am cautious to begin the year. I see the 1Q being a bit volatile, owing to the market interpreting and digesting what will likely be the beginning of a rate cut cycle. But to reiterate, I see 6 cuts as being overly optimistic at this point. The risks as Powell says himself are two sided. The war on inflation is not over, however the FOMC also doesn’t want to completely ignore the risks to the economy as well. On a price action basis, I am expecting a test again of last years summer high of 4600. I think the narrative for that is somewhere along the lines of a hotter jobs number NFP, or possibly a hawkish Powell “correcting” the exuberance the rates market has been pricing in the last week of January. As it stand right now, barring new significant information, I am leaning to buy that dip. I see us traversing to and through SPX 5000 sometime in the Summer. As is typical, August-October we most likely see some weakness and risk-off, especially as we rapidly approach the 2024 Presidential election. I don’t think its sensationalist to say this will be the most important election to date.

There are a myriad of polls circulating out there, but most of them show the same general trend. Approval for Joe Biden is very low, and at the lows. Meanwhile, Trump has his own fair share of problems. This is not a politics blog so I will leave it at that but it’s especially important to markets this year on multiple fronts. Regarding the deficit, fiscal policy, China/Taiwan, the Middle East, Russia/Ukraine, and the FOMC. There will also likely be drama surrounding mail in ballots, fair elections and the like. Expecting volatility in 3Q due to this.

Depending on the outcome of the election, we can potentially see a rally to 5300-5500 SPX. Coming off a strong 2023, I wouldn’t be surprised to see a solid 15% gain this year. That would be my base case this year, I assign to it maybe a 60% probability. On the other hand, the main risk remains the same for markets this year. The inflation boogeyman. Many fear the rapid easing in the Financial Conditions Index could spur a reigniting of inflationary pressures. The comparisons of Powell to Arthur Burns are present of course.

The same issues that were present in the throes of the third quarter bond selloff haven’t gone anywhere, they are still hiding under the bed. If we see CPI trend upwards meaningfully for a couple months, if we see escalation in the wars of the Middle East or Europe, if we see market pricing in another Joe Biden term along with out of control spending, the risk is a break upwards of the 5% yield barrier.

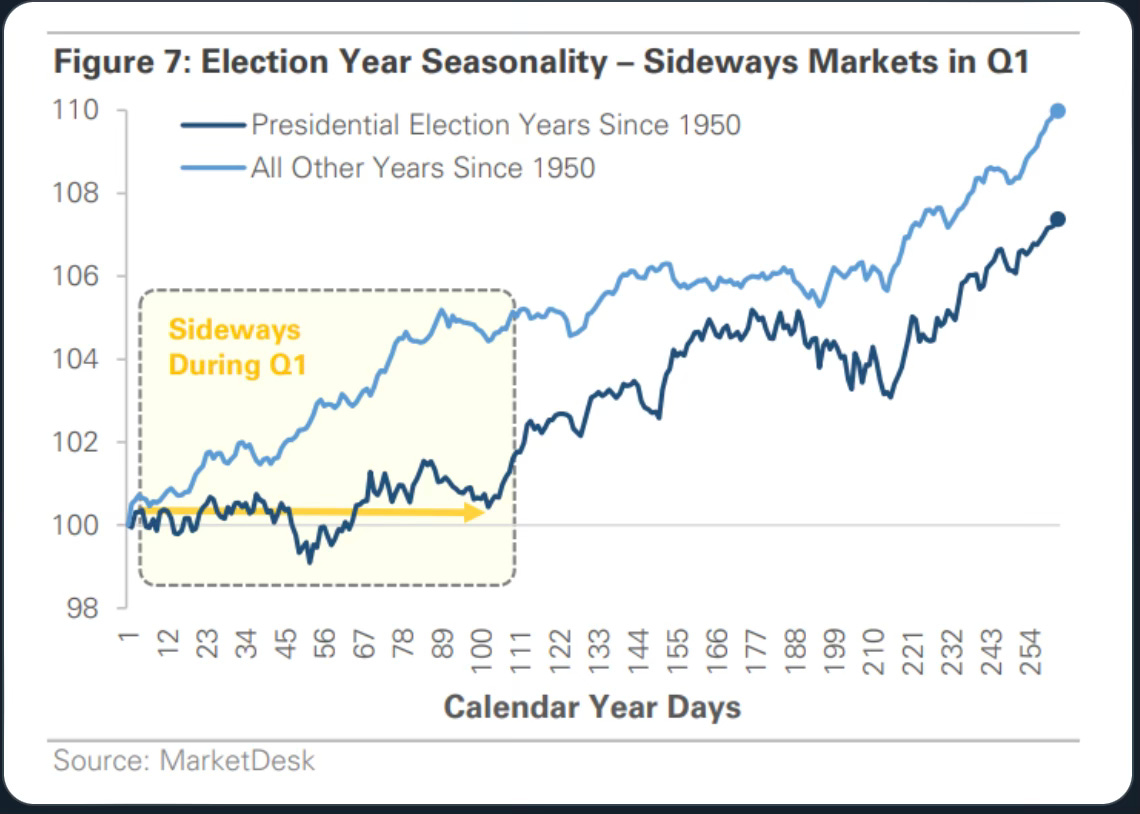

Generally speaking, I am bullish on equities again in the year 2024. I think 1Q will be on the weaker side, primarily due to an overshoot of the markets pricing in of cuts. This extreme greed, high asset allocation, and extremely bullish sentiment are also short term headwinds. But like many bullish indicators, short term weakness does not preclude medium and long term strength. Election year also tends to have a distinct seasonality which supports my thesis.

I think the market starts to feel some gravity again by latest end of Jan as I think Powell wants to reign in speculation a bit. However, after a bit of accumulation and some more volume transacting in this 4600+ range, I see us breaking 5000. 5300-5500 could come 4Q as begin a new Presidential cycle. One of the major drivers here will be this jaws gap closing. With rate cuts, comes falling yields, and that money will be searching for a more robust return than 3-4%. Especially if equities are making new highs.

This bullish thesis goes out the window in a couple scenarios. First and foremost is if we get a resurgence of inflation. In that case, this gigantic bond rally would be only a bear market rally, and we would likely test new highs in yields. That is definitely possible, but I dont want to go front-run the less likely doom and gloom scenario. I will start trading that scenario when I start to see a trend of data confirming it, not before.

Secondly, is the US experiences a recession. Much like the above scenario, I think the mistake to avoid here is front-running the doom scenario when you are not sure when it comes, or if it ever comes. If we do enter a recession, the data will foreshadow it well in advance. I see some signs of poor soft data, mainly ISM surveys and consumer confidence but the hard data (GDP, jobs, retail sales) is not confirming the trend so far. No recession on the horizon with the Unemployment Rate at ~3.7%. Period.

To conclude, I am bullish until proven otherwise. I am expecting something like a 4500-5500 range to play out in 2024. Unless we see a recession, which we will first need to see reflected in the jobs data (ADP and NFP specifically). Or unless we see inflation reaccelerate (CPI and PCE specifically). The first half of the year will be about pricing in cuts and The Fed, the second half more focused on the election, and what that means for future policy (think fiscal, monetary, tax, China, Mexico, energy, NATO, etc).

This is where my head is at currently, things can change at any time with new information and they probably will. Expect the unexpected.